Fund spotlight: Vitality Investec Multi-Asset Fund

Responding to market volatility

Published: 18/03/2020

This site is for UK investment professionals only. If you're

not an investment professional, please find out more about us at vitality.co.uk

The coronavirus (COVID-19) has continued its spread across the world, with unpredictable consequences for society, business and financial markets. Given the current volatility, John Stopford and Jason Borbora-Sheen, portfolio managers of the Vitality Investec Multi-Asset Income Fund (“the Fund”), explain their intentions for navigating the Fund through an uncertain and rapidly evolving situation.

The Fund has proved its resilience in the face of negative market pressure in the past, and the portfolio managers apply a consistent, tried and proven approach for protecting capital in a downturn.

In this note, they outline the most up-to-date summary of markets, how the portfolio is accordingly positioned, any significant changes to the portfolio given latest developments and an insight into how they have navigated similar drawdown periods in the past.

Market summary

Stock markets have sold off sharply since 20 February, experiencing the fastest correction on record, as the spread of the coronavirus outside of China has resulted in the World Health Organisation classifying the virus as a global pandemic.

Almost all Growth assets have generated a negative return, hit by recession concerns due to the coronavirus spread outside of China. Oil has declined further into bear territory reflecting concerns that the virus could drag down global demand and the reluctance of Saudi Arabia and Russia to cut supply.

Equities across the board have extended their flight from risk with indiscriminate selling fuelled by passive investors, although certain sectors have fared particularly poorly such as travel companies, oil stocks and banks.

Credit has also been challenged with spreads increasing in both European and US high yield. Similarly, many assets which investors sought for defence have disappointed, with gold generating a negative return in February, for example.

Flows into the US bond market have seen the 10-year and 30-year Treasury yields drop to record lows. Within currencies, the US dollar has strengthened, and the Japanese yen has rallied strongly versus the US dollar.

Portfolio Positioning

In volatile times like these, a security-level bottom-up process means better visibility as to how each position should behave. We then combine this with pre-emptive asset allocation decisions, as we did in February:

- Hedged more than half of total equity exposure to protect the portfolio in the event of further declines. Our equity call options will cause our exposure to fall relatively quickly in the event of further market declines, while ensuring we’re able to participate in market upside

- We are beginning to tentatively, and highly selectively, add high yield in weakness as the market has become increasingly dislocated, and it is starting to look attractive again. We remain cautious however in current markets

- Emerging market bond exposure remains short duration, with currency risk largely hedged back to base

- Very little active currency risk, with some long Japanese exposure offering the portfolio strong defensive characteristics in these difficult times.

This combination of bottom-up fundamental research with pre-emptive asset allocation is consistent with how we have navigated similar draw-down periods before (see below for detail).

Portfolio Activity

Activity in February and March has been consistent with our bottom-up and top-down process. Our hedging process caused the Fund to decrease exposure to equities quickly during February as the most recent bout of volatility began. Our net equity fell from c.25% to currently c.7.5%.

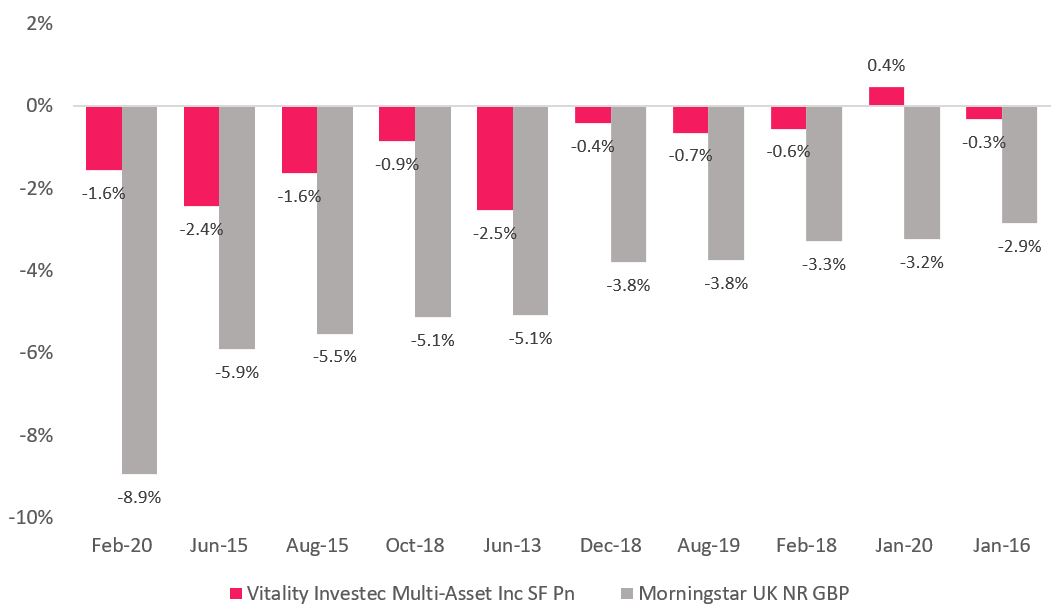

A defensive approach has led to lower downside capture

The defensive investment approach adopted by the Fund has once again proved its worth. The chart below shows how it has managed to withstand the worst of the market’s drawdown.

Returns during worst months of FTSE All Share*

The periods above have been picked based on the largest 10 single-month losses for FTSE All Share since inception of the Investec Diversified Income R, Acc, GBP share class – the underlying fund on which the VitalityInvest Multi-Asset Income Fund is based.

*Source: Morningstar and VitalityInvest, from 01 Sep 2012 to 29 February 2020. The Vitality Investec Multi-Asset Income Fund launched on 29 May 2018. Before this date, performance data is based on the actual past performance of the underlying Investec fund, Investec Diversified Income R, Acc,

GBP share class.

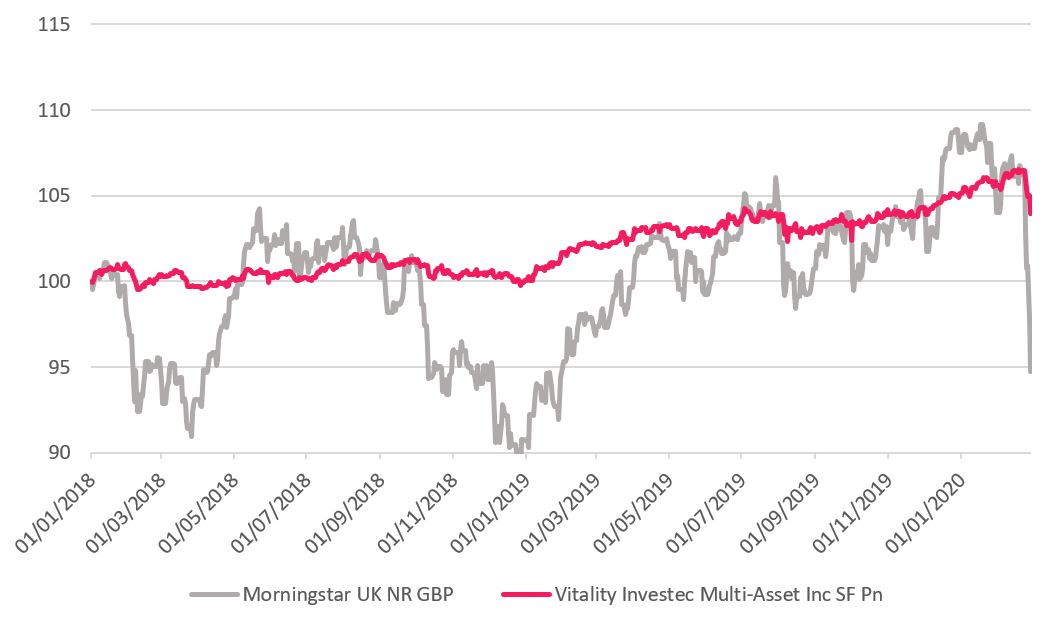

Returns during the different market environments of 2018, 2019 and YTD 2020

Past performance is not a reliable indicator of future results.

This performance data includes simulated past performance of the actual past performance of the underlying Investec fund, Investec Diversified Income R, Acc, GBP share class. While the Vitality Investec Multi-Asset Income Fund launched on 29 May 2018, the Investec Diversified Income Fund R, Acc, GBP share class launched on 2 January 2013.

Source of data: VitalityInvest and Morningstar, 13 March 2020. Performance is net of fees (NAV based, including ongoing charges, excluding initial charges), gross income reinvested, in GBP.

A longer-term perspective:

It is important to remember that the Fund is seeking not just to limit drawdowns but also to participate in upside. The last three years have seen remarkable asset class moves: 2018 was the worst year for markets since the financial crisis and saw bonds fail to provide protection in its most serious sell-off; 2019 then saw a potent reversal with best year for equities since 2009; now 2020 is seeing the fastest correction on record for the S&P 500. Over this period the Vitality Investec Multi-Asset Fund has outperformed equities with minimal relative volatility and drawdown.

General risks:

The value of investments, and any income generated from them, can fall as well as rise. Where charges are taken from capital, this may constrain future growth.

Past performance is not a reliable indicator of future results. If any currency differs from the investor's home currency, returns may increase or decrease as a result of currency fluctuations.

Investment objectives and performance targets are subject to change and may not necessarily be achieved, losses may be made.

Specific risks:

- Currency exchange: Changes in the relative values of different currencies may adversely affect the value of investments and any related income.

- Default: There is a risk that the issuers of fixed income investments (e.g. bonds) may not be able to meet interest payments nor repay the money they have borrowed. The worse the credit quality of the issuer, the greater the risk of default and therefore investment loss.

- Derivatives: The use of derivatives may increase overall risk by magnifying the effect of both gains and losses leading to large changes in value and potentially large financial loss. A counterparty to a derivative transaction may fail to meet its obligations which may also lead to a financial loss.

- Emerging markets: These markets carry a higher risk of financial loss than more developed markets as they may have less developed legal, political, economic or other systems.

- Equity investment: The value of equities (e.g. shares) and equity-related investments may vary according to company profits and future prospects as well as more general market factors. In the event of a company default (e.g. insolvency), the owners of their equity rank last in terms of any financial payment from that company.

- Government securities exposure: The Fund may invest more than 35% of its assets in securities issued or guaranteed by a permitted sovereign entity, as defined in the definitions section of the Fund’s prospectus. Interest rate: The value of fixed income investments (e.g. bonds) tends to decrease when interest rates rise.

Important Information

This document was written by Ninety One (formerly Investec Asset Management). VitalityInvest takes no responsibility for any inaccuracies or errors in the content of the document.

This document is being provided for informational purposes for discussion with institutional investors and financial advisers only. Circulation must be restricted accordingly.

Nothing herein should be construed as an offer to enter into any contract, investment advice, a recommendation of any kind, a solicitation of clients, or an offer to invest in any particular fund or plan.

This document may not be reproduced or circulated without prior permission. No statements or representations made in this document are legally binding on VitalityInvest or the recipient.

This information is not a personal recommendation for any particular investment or course of action.

The content of this article is always subject to the Key Features and Terms and Conditions for our VitalityInvest plans.

The value of investments and the income from them can go down as well as up and your client may get back less than they invest.

To find out more, please see the Key Features/Plan Summary and Terms and Conditions for our VitalityInvest plans.

VitalityInvest is a trading name of Vitality Corporate Services Limited. Vitality Corporate Services Limited is authorised and regulated by the Financial Conduct Authority.

17/03/2020 | This article’s view is based on the law, practices and conditions as at the day of publication. While we have made every effort to ensure they are accurate, we accept no responsibility for our interpretation or any future changes. |